Editor's Note: Kevin Warsh's appointment as Chairman of the Federal Reserve impacts far more than just a personnel change; it signifies a shift in the market's pricing logic itself. Under Warsh's framework, inflation is being reinterpreted as a problem of fiscal indiscipline and government inefficiency, while AI is seen as a key tool for reducing costs, boosting productivity, and reshaping governance capabilities.

As AI systems like Palantir are being deployed in areas such as federal spending audits, housing finance, and medical reimbursements, this institutional shift is moving from concept to execution and is manifesting in the market as structural differentiation and repricing.

With AI and fiscal discipline becoming the main policy themes, the question of which assets will command a new pricing premium and which business models will face systemic revaluation is becoming a question the market must answer. The original text follows:

The appointment of Kevin Warsh as the new Chairman of the Federal Reserve sends a signal that goes far beyond a personnel change; it heralds a deep-seated shift in global monetary policy paradigms and the AI arms race. The connection between these two is far more profound than most realize.

AI is becoming the only asymmetric leverage point that will determine the future landscape, and Warsh's appointment is an institutional arrangement centered around this core objective.

Discussions about him—such as "Will he cut rates?", "Is he a hawk or a dove?", "How will he handle the Fed's balance sheet?"—are certainly important, but they all overlook one fact: a larger institutional transition is already underway.

The truly critical issue is not short-term policy orientation, but why it is Kevin Warsh and how he fits into this newly forming system. Understanding this will be the most important variable heading into 2026.

From Personnel Appointment to Institutional Signal: Why Warsh?

Warsh is not a traditional "policy technocrat." He has long been seen as someone with a systemic understanding of global capital flows, financial market structures, and institutional incentives.

More importantly, he is not an isolated individual.

Warsh has long maintained close ties with Druckenmiller, Beeson, and Karp, all of whom have deep connections to Palantir. Druckenmiller has repeatedly publicly praised Warsh's ability to understand global capital flows and financial market structures.

In an interview with Bloomberg, Druckenmiller even called Warsh his "trusted advisor."

But the connection goes further: Druckenmiller himself is an early investor in Palantir and has a close relationship with its co-founder and CEO, Alex Karp. (Related reading: interview link)

Why is this important? Because Kevin Warsh himself has a direct connection to Palantir.

In 2022, Alex and Kevin recorded an interview discussing how the world is moving toward greater disorder and higher complexity.

As they stated in the interview: "Tomorrow, complexity will take a step-function leap."

This is not an empty statement of techno-optimism but a forward-looking judgment on the impending changes in national governance, fiscal systems, and methods of macroeconomic stability.

Palantir: The "Execution Layer" of Institutional Transition

Understanding Warsh requires understanding Palantir.

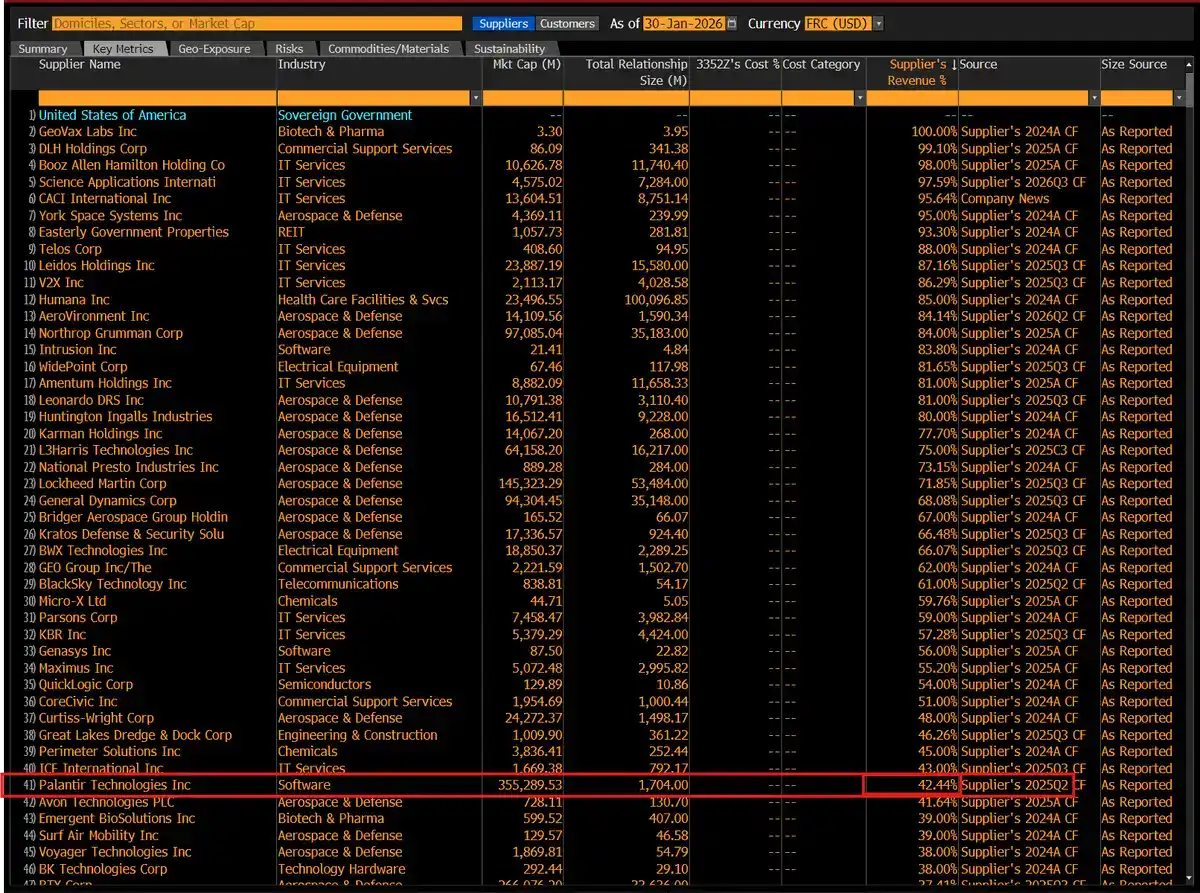

Palantir is crucial precisely because it is gradually becoming the "operational hub" of the U.S. federal government's anti-fraud system. Currently, 42% of Palantir's revenue comes from the U.S. government, and its technology is being deployed across multiple government agencies to identify and curb large-scale fraud and excessive, inefficient government spending.

Why is this important?

Because Palantir is being used to systematically address issues of excessive waste and various types of fraud in government spending. Its technology is being implemented in multiple federal agencies, becoming a key tool for identifying anomalous fund flows and eliminating redundant expenditures.

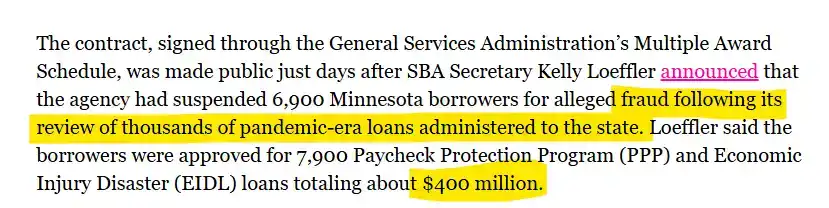

SBA: From a Single State to a National "Zero Tolerance" Crackdown

A most representative example comes from the U.S. Small Business Administration (SBA).

While investigating loan programs during the pandemic, the SBA discovered large-scale violations in Minnesota: involving 6,900 borrowers, approximately 7,900 PPP and EIDL loans, totaling about $400 million.

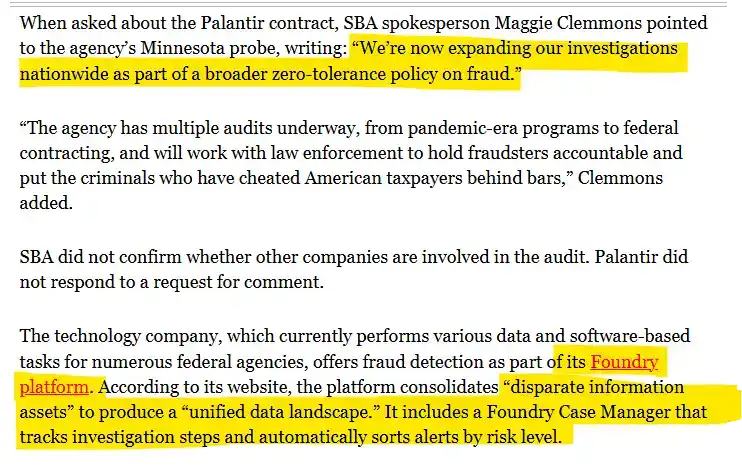

In this context, the SBA brought in Palantir and explicitly stated that the investigation would expand from a single state to a "zero tolerance" systemic anti-fraud action nationwide.

Relevant documents show that Palantir, through its Foundry platform, integrates government data scattered across different agencies and systems, tracks the investigation process, and prioritizes leads based on risk level. This means Palantir is no longer just providing analytical tools but is deeply embedded in the federal government's audit and anti-fraud workflow.

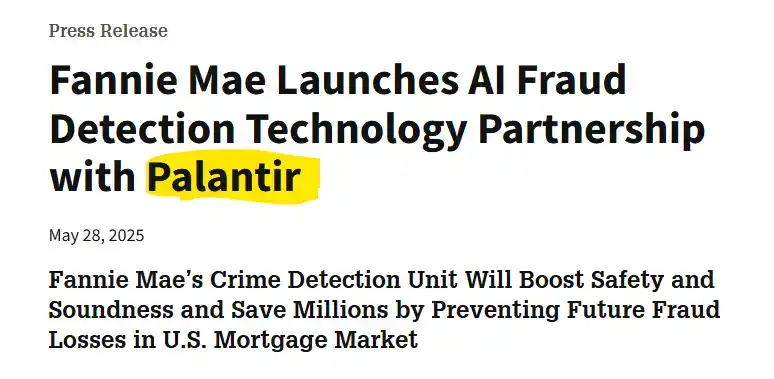

Fannie Mae: Systemic Pre-Audit of the Housing Finance System

A similar logic is unfolding in the housing finance system.

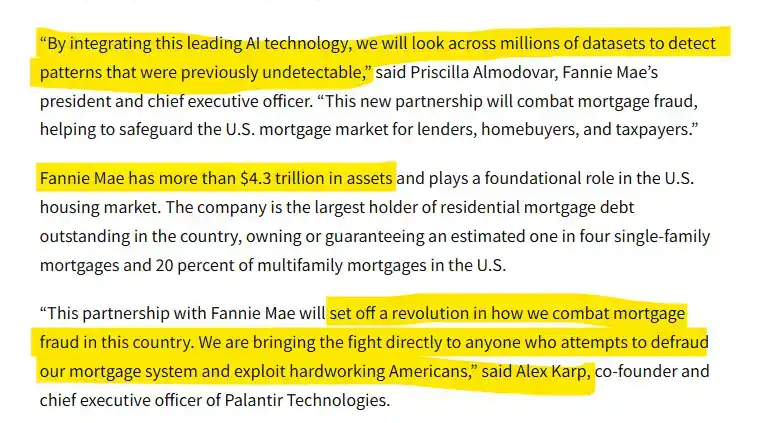

Fannie Mae has formally established an AI anti-fraud technology partnership with Palantir, integrating Palantir's AI capabilities into its crime detection system to identify previously undetectable fraud patterns in datasets comprising millions of records, thereby reducing future losses in the U.S. mortgage market.

The context of this partnership is particularly crucial: Fannie Mae manages over $4.3 trillion in assets and holds a foundational position in the U.S. housing finance system, covering nearly a quarter of single-family mortgages and 20% of multifamily mortgages. Fannie Mae emphasized that this move will enhance the safety and soundness of the entire mortgage market; Palantir CEO Alex Karp stated outright that this partnership will "change the way America fights mortgage fraud" by embedding anti-fraud capabilities directly at the system level.

So what is the "connection" between them? The answer lies in the fact that the federal government is increasingly deploying Palantir's anti-fraud capabilities across different domains.

This indicates that the "fiscal theory of inflation" advocated by Warsh is not merely academic but is being translated into executable, auditable, and accountable government capabilities through AI systems like Palantir.

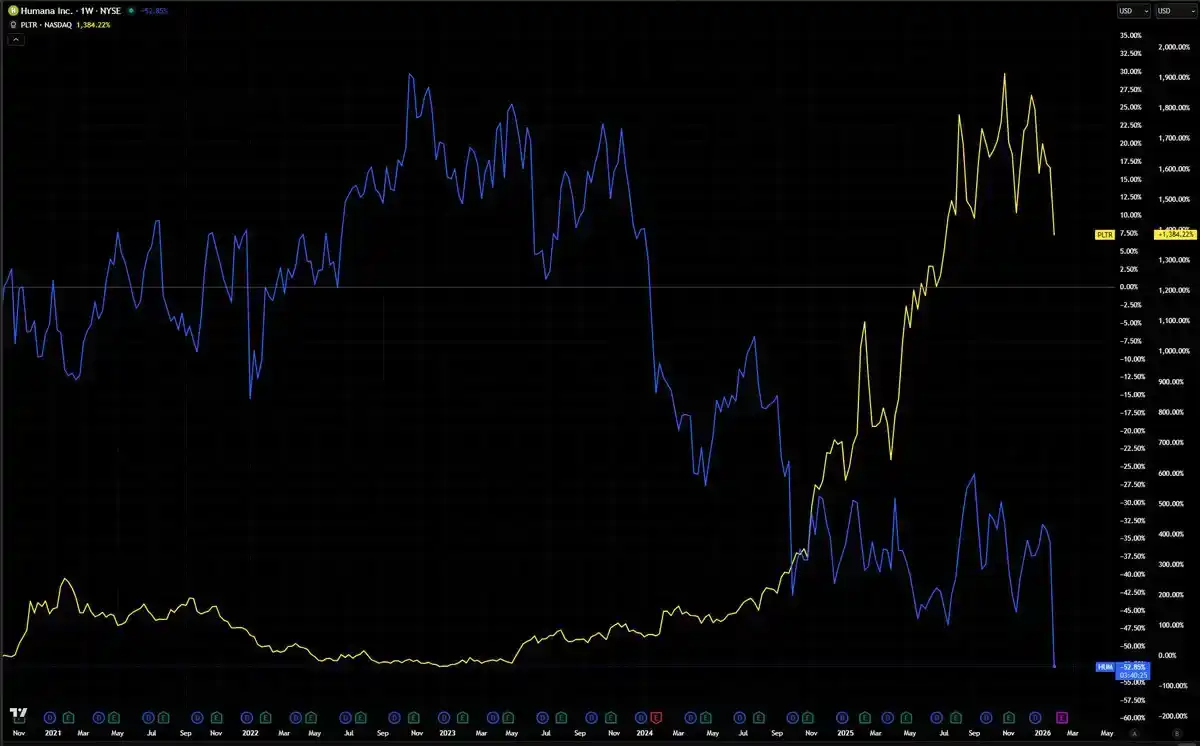

I find one phenomenon very interesting: Humana, a company with government contracts exceeding $100 billion, is one of the government's largest contractors, yet its stock price has been weakening even as Palantir's continues to rise.

Whether there is a direct correlation between these two stocks or not, this relative performance is noteworthy in itself. Humana's business model is largely built on the high complexity of the government medical reimbursement system—a complexity that has historically been difficult to audit on a large, systemic scale. In contrast, Palantir is being deployed precisely to introduce transparency into such programs.

This divergence may be signaling a more macro message: the market is repricing two types of companies—those that benefit from opacity and those that provide visibility and transparency. If AI-driven regulation and auditing become the norm for federal fiscal expenditures, this structural change will likely occur not only in healthcare but across more industries.

When AI Meets Inflation: Why This is an Institutional Shift

Kevin Warsh has been advocating for an "institutional change" at the Federal Reserve for over a decade. But what does that actually mean?

The answer begins with a completely different theory of inflation.

The inflation models currently dominant within the Fed were largely developed in the 1970s and remain in use today. These models posit that inflation arises from an overheating economy and excessively rapid wage growth.

Warsh completely rejects this explanation. In his view, the root of inflation lies not in wages but in the government itself—when the government prints too much, spends too much, and becomes too "comfortable," inflation occurs.

This view is not implied; it is a position he has explicitly stated multiple times.

This is the true "institutional change." It is not about whether the Fed is hawkish or dovish, nor whether it raises or cuts rates by 25 basis points. The key is to completely rewrite the Fed's inflation analysis framework, shifting from a theory that attributes inflation to workers and economic growth to one that holds government spending itself accountable.

This is where it gets interesting.

Warsh is also highly optimistic about AI. In the same interview, he pointed out that AI will lower the cost of almost everything and that the U.S. is on the cusp of a major productivity explosion. He believes the current Fed fails to see this, constrained by old models, and mistakes economic expansion for inflation.

Thus, on one hand, Warsh sees AI as a structural deflationary force that will continuously压低 costs throughout the economy; on the other hand, he believes the true source of inflation is excessive government spending and fraud—where large amounts of money are injected into the system without corresponding real output.

And these two seemingly different judgments converge at the same node: Palantir.

In fact, this institutional shift does not just reshape the Fed itself; it reorders the entire framework through which we understand interest rates, the dollar, and global capital flows.

If Warsh's judgment is correct—that inflation stems primarily from fiscal expansion, not supply-side shocks—then the traditional macroeconomic playbook becomes utterly obsolete.

In this framework, cutting rates no longer signifies a dovish stance but rather indicates policymakers' confidence that fiscal discipline and AI-driven efficiency gains are taking on the primary task of curbing inflation. The Fed is no longer the antagonist of fiscal constraint but its collaborator.

A Fed that refuses to monetize fiscal deficits while actively supporting the reduction of fraud and the compression of spending will create a monetary regime entirely different from the environment markets have priced in over the past decade.

This is also significant globally. If the U.S. can demonstrate that AI can be deployed at scale to strengthen fiscal accountability—including cutting waste, identifying fraud, and streamlining government operations—then this model will either be emulated by other developed economies or become a standard they must compete against.

The so-called AI arms race is not just about chips or model capabilities; it is about who can率先 use AI to重塑 the relationship between government and the economy.

Additionally, there is the deflationary force brought by AI itself. Warsh's position is very clear: he believes AI will压低 costs across the economy and that we are on the eve of a productivity explosion, something the current Fed has yet to fully grasp.

If his assessment holds, we will enter an unprecedented phase: structural forces are deflationary (productivity gains from AI), while the source of inflation is directly targeted and suppressed (government waste and fraud). This would constitute an investment environment not seen since the 1990s.

Old thinking frameworks—hawk vs. dove, rate hikes vs. cuts, risk-on vs. risk-off—are insufficient to explain the changes underway.

The real question for 2026 is not where the federal funds rate lands, but whether this alliance truly possesses the ability to execute its grand vision.

How Will Markets Be Repriced After the Institutional Shift?

Kevin Warsh will become the next Chairman of the Federal Reserve. Markets may instinctively categorize him as a "hawk," but this understanding is inaccurate. As we truly enter 2026, Warsh's policy stance will present more complex and structural characteristics.

Below are the main policy directions he is likely to promote and the potential impact of these changes on different asset classes:

· AI / Semiconductors ($NVDA, $MU): Extremely Bullish

· Metals (Silver, Gold): Extremely Bearish

· Crypto Assets ($BTC, $CRCL): Superficially Contradictory, Actually Leaning Bullish

· Banking & Financial Sector ($JPM, $BOA): Bullish

· Housing & Real Estate: Divergent / Uncertain

· Renewable Energy: Bearish

· Small-Cap Stocks ($RUT): Bullish

· International Equities:

Japan, South Korea: Relatively Resilient

Emerging Markets (EM): Under Significant Pressure

China & Hong Kong: Leaning Bearish

Europe ($VGK, $EZU): Cautious View

AI / Semiconductors (From NVIDIA to Micron): Extremely Bullish

Warsh is an explicit and consistent AI bull.

In late 2025, he publicly stated that AI is a powerful structural "disinflationary" force. In his view, the productivity leap brought by AI can allow the economy to maintain high growth rates without necessarily pushing up inflation.

It is this judgment of a "productivity boom" that provides a solid theoretical foundation for him to support rate cuts even without significant economic cooling.

("Federal Reserve Leadership Failure," The Wall Street Journal, November 16, 2025)

This stands in stark contrast to the market's previous stereotype of him—Warsh was often seen as a rigid, high-rate, anti-inflation hawk.

Now, he not only supports rate cuts but explicitly hopes to accelerate the deployment and expansion of AI.

Metals (Silver, Gold): Extremely Bearish

Gold has long been seen as a hedge against a weakening dollar and monetary excess. But under Warsh's policy framework, this logic is being undermined.

He advocates shrinking the Fed's balance sheet and ending "printing-press easing," directly challenging the core rationale for holding gold. Simultaneously, a strong dollar further increases the cost of metals for international buyers.

It should be added that silver's 33% intraday plunge was primarily driven by technical factors like margin adjustments triggering连锁 liquidations; the influence of the new Fed Chair is likely a secondary driver.

Crypto Assets ($BTC, $CRCL): Superficially Contradictory, Actually Leaning Bullish

Warsh has直言: "If you are under 40, Bitcoin is your new gold." In his view, Bitcoin is a legitimate store of value, representing an intergenerational shift from physical precious metals to digital assets.

He also highly praises blockchain, calling it the "newest, most disruptive foundational software," and believes the U.S. must lead in this field to maintain long-term competitiveness.

But the question is: if the stance is bullish, why is the price under pressure? The reason is that the market is gradually realizing: while Warsh supports lower policy rates, he simultaneously insists on balance sheet reduction and monetary discipline.

This raises a new concern—we might be entering an era of "rate cuts, but without accompanying QE." Borrowing costs may fall, but the "liquidity deluge" that has repeatedly pushed Bitcoin to new highs may not reappear.

Thus, a tension exists: Warsh is bullish on crypto assets from a technological and long-term trend perspective, but his monetary restraint may suppress liquidity premiums in the short term.

Banking & Financial Sector: Bullish

With his background at Morgan Stanley and long-standing criticism of regulatory "mission creep," Warsh has always been a policy preference for the banking system. The market widely expects him to roll back some complex bank capital requirements (e.g., Basel III).

Analysts believe this will significantly benefit regional and community banks, as more capital will be released for实体 credit expansion.

Housing & Real Estate: Divergent

Warsh advocates significantly lowering the federal funds rate, which would directly reduce the cost of Adjustable-Rate Mortgages (ARMs) and construction financing.

But the risk is: he explicitly opposes the Fed holding roughly $2 trillion in Mortgage-Backed Securities (MBS). Many economists warn that even if other rates fall, the 30-year fixed mortgage rate could still be pushed into the 7%–8% range.

Renewable Energy: Bearish

Warsh plans to have the Fed withdraw from global climate-related organizations (like the "Network for Greening the Financial System") and terminate climate stress tests for banks.

Under Powell's tenure, the Fed used regulatory guidance to encourage banks to incorporate climate considerations into credit. Warsh wants to end this mechanism, effectively removing the "policy tailwind" previously enjoyed by green projects.

Small-Cap Stocks: Bullish

Warsh has repeatedly emphasized that the Fed should refocus on the true drivers of the economy—small businesses and entrepreneurs—not "the over-protected large institutions on Wall Street."

He is expected to push for a systematic rollback of bank regulation, which directly benefits small-cap stocks. By减轻 the regulatory burden on small and medium-sized banks, the渠道 for SMEs to obtain financing will be significantly widened.

International Equities: Divergent

Warsh's policy mix could create significant divergence globally: one group of economies will benefit from U.S. growth and AI investment; another will be more susceptible to pressure from a strong dollar and tighter global liquidity.

Japan / South Korea (e.g., Samsung, SK Hynix): Relatively resilient because they control key physical bottlenecks in the AI and robotics industries, precisely the productivity engines Warsh values.

In this context, a strong dollar becomes a competitive tool for them:

Export Effect: Contracts are mostly dollar-denominated, significantly放大 profits upon currency conversion;

Cheaper from a U.S. Perspective: A stronger dollar makes Japanese robots and Korean chips more price-attractive to U.S. companies, accelerating productivity gains while enhancing these firms' profitability.

China:

A strong dollar will continue to pressure the Renminbi, limiting the room for monetary policy maneuvering.

Emerging Markets:

Dollar appreciation significantly increases the burden of dollar-denominated debt, exacerbating risk exposure.

Europe:

A weaker euro benefits exports, but rising energy import costs pose a structural constraint.

Last Friday, the plunge in silver and gold triggered hedging and de-risking behavior, leading to a temporary tightening of liquidity.

The market may still simplistically categorize Warsh as a "traditional hawk," but based on his recent statements, in the short term he appears closer to a "dovish proponent predicated on AI."

The market is currently digesting a new combination of circumstances: rate cuts occurring alongside balance sheet contraction.

Within this framework, multiple trading logics, from the AI theme to small-cap growth, are still seen as having continuity.